Climate Tech Investment Defies Skeptics as IEA Revises Outlook

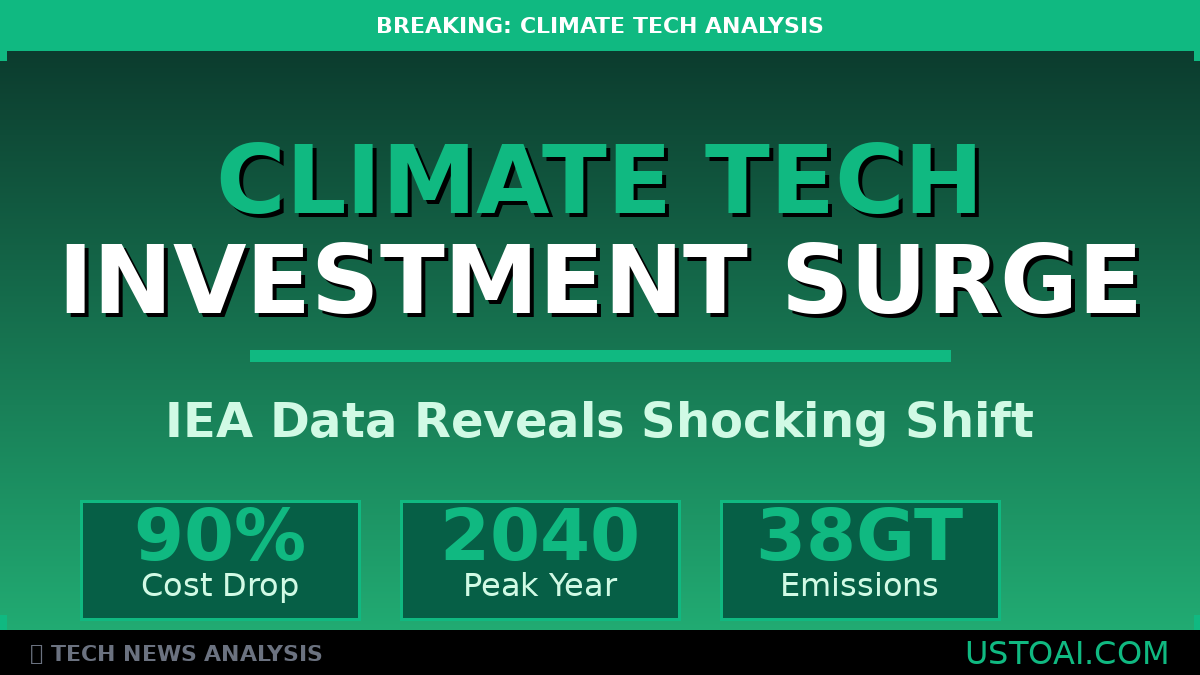

The numbers tell a story climate tech investors didn’t expect to hear in 2025. A decade ago, the International Energy Agency projected global carbon emissions would climb relentlessly toward 46 gigatons annually by 2040, even under the most optimistic scenarios. Policy pledges and technological advances might bend that curve slightly downward—to perhaps 38 gigatons—but the trajectory pointed in only one direction. This week’s IEA World Energy Outlook turns that projection on its head. The agency now expects emissions to plateau around 38 gigatons under current policies, with pledged commitments potentially driving them down to 33 gigatons by 2040. Yesterday’s best-case scenario has become today’s business-as-usual forecast. For an industry that spent much of 2024 navigating what venture capitalists euphemistically call “market corrections,” the revised outlook arrives at an inflection point. Climate tech funding fell sharply from 2021 peaks. Political headwinds intensified. Yet beneath the pessimism, something fundamental shifted in how quickly clean technology penetrates global markets.

When the Worst Case Becomes the Best Case

The gap between 2014’s projections and 2025’s reality reveals more than forecasting error. It exposes how dramatically the economics of clean energy transformed in barely a decade. Solar panel costs dropped roughly 90% since 2010. Wind power became the cheapest electricity source in most markets. Battery prices fell by similar margins, making grid-scale storage economically viable for the first time. These aren’t incremental improvements. They’re the kind of cost curves that rewrite industry assumptions—and they happened faster than most analysts predicted. “We systematically underestimated the pace of technological learning,” admitted one former IEA analyst who requested anonymity to speak candidly about the agency’s earlier projections. “The feedback loops between deployment, manufacturing scale, and cost reduction proved much stronger than our models suggested.” China’s role in accelerating those feedback loops cannot be overstated. The country now manufactures roughly 80% of global solar panels and dominates battery production. That industrial capacity didn’t just lower costs—it fundamentally changed what’s possible.

The Investment Case Nobody Expected

Conventional wisdom holds that climate tech entered a prolonged winter after the 2021 funding surge. Valuations compressed. Late-stage rounds became scarce. Several high-profile startups stumbled or shut down entirely. But aggregate funding numbers obscure a more nuanced picture. While total climate tech investment declined from record highs, capital flowing into specific technologies—particularly those addressing data center energy demands and grid optimization—actually increased year-over-year. The distinction matters. Early-stage hardware companies chasing billion-dollar exits face difficult fundraising environments. But software startups solving immediate grid reliability problems, or firms deploying proven technologies at scale, found receptive investors willing to write checks. “The market matured,” explained Sarah Chen, managing partner at a Bay Area climate fund that closed $400 million in commitments this year. “Investors stopped chasing moonshots and started backing companies with clear paths to profitability. That’s actually healthier for the sector long-term.” Germany’s electric vehicle market illustrates this maturation. EV sales hit new records in 2024 and 2025 despite the government eliminating purchase subsidies in late 2023. The vehicles became competitive on their own merits—lower operating costs, better performance, expanding charging infrastructure—rather than requiring policy support to drive adoption. Similar patterns emerged across technologies. Renewables won power contracts in developing nations not because of climate commitments but because they offered the cheapest electricity available. Corporate purchasers signed long-term agreements for clean power to hedge against fossil fuel price volatility, not primarily for sustainability reporting. When clean technology competes on economics rather than subsidies, it unlocks demand that policy mechanisms alone cannot create.

The Geothermal Wildcard

The IEA’s updated projections incorporate steady growth in solar, wind, and battery storage—technologies with established deployment trajectories. They do not, however, fully account for potential breakthroughs in next-generation geothermal or AI-optimized grid management systems that several startups are piloting. Advanced geothermal techniques adapted from oil and gas drilling could unlock vast quantities of clean baseload power. Companies like Fervo Energy and Eavor demonstrated the technical viability. The question is whether they can scale production and drive costs down quickly enough to matter for 2030s deployment. Machine learning systems optimizing grid operations present similar upside potential. Startups applying sophisticated algorithms to balance variable renewable generation have already demonstrated they can squeeze additional capacity from existing infrastructure—effectively creating new supply without building new plants. If these technologies follow anything resembling the cost curves that solar and batteries traveled, they could accelerate emissions reductions beyond what current models predict. The IEA’s 2025 outlook might prove as conservative as its 2014 version, just in the opposite direction.

China’s Unexpected Climate Pivot

Perhaps the most significant shift in the past decade involves China’s carbon trajectory. For years, China insisted it would not peak emissions until at least 2030 and potentially much later. The country prioritized economic growth over climate commitments, and analysts expected carbon output to rise accordingly. Recent statements from Chinese officials suggest a different path. The government now projects emissions will peak before 2030—potentially within the next few years. That represents a fundamental revision to the outlook for global emissions, given China accounts for roughly 30% of worldwide carbon output. What changed? The economics became compelling. China recognized it held dominant positions in the manufacturing supply chains for clean energy technologies. Accelerating the global transition to renewables and EVs plays to Chinese industrial strengths while reducing dependence on imported fossil fuels. Geopolitical strategy and climate policy aligned in ways that pure emissions reduction targets never achieved. Whether motivated by environmental concerns or industrial policy, the practical effect is the same: the world’s largest emitter moving toward peak carbon years ahead of schedule.

The Trend Within the Trend

Forecasting carbon emissions requires making assumptions about technology costs, policy decisions, economic growth, and countless other variables. Get any major assumption wrong and projections diverge from reality. The IEA’s 2014 forecast missed badly on technology costs. Solar and batteries became cheap faster than models predicted. That single variable—cost reduction—cascaded through the entire projection, rendering it obsolete within years. Looking at 2025 projections through that lens raises an obvious question: what assumptions might prove equally wrong this time? The most likely candidate is deployment speed. Once technologies become cost-competitive, adoption often accelerates in ways linear models fail to capture. Markets tip. Supply chains mature. Institutional knowledge accumulates. Feedback loops intensify. We’ve already seen this pattern with smartphones, which went from niche devices to ubiquitous in barely a decade. AI adoption followed similar trajectories, with ChatGPT reaching 100 million users in two months—a speed unthinkable even five years ago. Clean energy technologies may be entering their own adoption acceleration phase. Electric vehicles in Norway now represent over 90% of new car sales. Heat pumps are becoming standard in new European construction. Grid-scale batteries are being deployed at scales that seemed far-fetched half a decade ago. If deployment continues accelerating rather than following linear growth patterns, emissions could decline significantly faster than current projections suggest. The question is whether investors recognize the opportunity before it becomes obvious to everyone.

What This Means for Climate Tech Investing

The paradox facing climate tech investors is that the sector’s biggest successes may have already occurred. Solar and batteries won. The technologies work. Costs came down. Markets tipped toward adoption. What’s left to invest in? The answer lies in the gap between today’s infrastructure and tomorrow’s requirements. The grid needs massive upgrades to handle variable renewable generation. Buildings require retrofits for electrification. Industrial processes need to be reimagined around clean energy inputs. Supply chains must be reorganized. None of these challenges have obvious technological solutions waiting to be deployed at scale. They require innovation in business models, software, systems integration, and manufacturing processes. The opportunities are less flashy than breakthrough battery chemistries or fusion reactors, but potentially more impactful. For investors willing to back companies solving these pragmatic challenges, the updated IEA outlook provides validation. The world is moving faster than expected toward clean energy adoption. That creates enormous demand for the picks and shovels of the energy transition—even if those tools look more like grid management software than revolutionary hardware. The climate tech winter that venture capitalists feared may be more accurately described as a maturation. Hype cycles ended. Business models hardened. The sector is growing up, which means getting boring in all the right ways.

The Political Question Mark

One variable complicates this relatively optimistic picture: policy uncertainty. The IEA’s projections assume countries follow through on existing commitments. Recent political shifts in several major economies raise questions about that assumption. US climate policy faces potential reversals depending on election outcomes. European commitment to the Green Deal wavered amid energy security concerns following Russia’s invasion of Ukraine. Developing nations continue prioritizing economic growth over emissions reductions when the two conflict. Yet technology economics may matter more than policy. Germany’s EV adoption continued accelerating after subsidy removal. Corporate clean energy purchasing grew even as policy support plateaued. Market forces increasingly drive decisions that climate policy once had to incentivize. The question is whether that dynamic holds when economic conditions deteriorate or energy prices spike. Technology costs fell during a period of relative stability and low interest rates. Whether those trends survive economic stress remains untested.

Reading the Signals

Investors face a choice in how to interpret the gap between 2014 projections and 2025 reality. One reading suggests the IEA systematically underestimates technological progress, implying current projections may prove equally conservative. The alternative interpretation is that the past decade represented an anomalous period of rapid cost declines that won’t repeat. The truth likely lies somewhere between those extremes. Some technologies—particularly solar and batteries—probably extracted most available cost reductions from manufacturing scale. But other technologies—geothermal, grid software, green hydrogen—sit earlier on their cost curves with significant room for improvement. For climate tech investors, that distinction matters enormously. Backing mature technologies offers lower risk but modest returns. Betting on emerging technologies carries higher risk but potentially transformative upside if they follow the cost trajectories that solar and batteries demonstrated. The updated IEA outlook doesn’t resolve that uncertainty. It does, however, provide evidence that technology-driven emissions reductions can happen faster than conventional wisdom suggests—which may be the most important signal of all for investors trying to time entry into the sector. The question isn’t whether to invest in climate tech. It’s whether you trust the rate of change to accelerate or revert to historical norms. How you answer that determines whether now looks like the best time to invest, or whether you’ve already missed the opportunity.

Key Takeaways

• IEA’s 2025 worst-case emissions scenario matches 2014’s best-case projection, showing dramatic shift in expectations • Solar and battery costs fell 90% in a decade, exceeding forecasters’ predictions and reshaping energy economics • Germany’s EV sales hit records after subsidy removal, suggesting technologies reached economic competitiveness • China now expects emissions to peak before 2030, years ahead of previous projections • Climate tech funding shifted from speculative hardware to proven deployment and grid optimization software • Next-generation geothermal and AI grid management could accelerate emissions reductions beyond current models

Originally published at USTOAI — Your source for technology and business analysis.Follow us for more insights on technology trends shaping energy, climate, and infrastructure markets.

Related Reading: • DeepSeek Shakes AI Industry: China’s $6M Model Challenges Silicon Valley • Google Gemini 3 Breaks AI Benchmarks as Tech Giants Race for Supremacy • How Does ChatGPT Make Money? Inside OpenAI’s $2 Billion Business Model

Sources: International Energy Agency, TechCrunch, Reuters, New York Times, industry analysts